This blog describes how a Hybrid Domestic Asset Protection Trust (DAPT) works for grantors wanting an escape clause while taking advantage of their $11.7 million estate tax exemption (as of Jan 2021). This post will cover:

The rush in 4Q2020 to move assets out of people’s estate was prudent. How many added an escape clause to these trusts? As practitioners found out 8 years ago in 2012, that changes to the estate tax exemption are off the bottom not the top. The escape clause, within a Hybrid Domestic Asset Protection Trust (DAPT) allows the grantor to make a request with the trust protector to be added as a beneficiary, though through a different trust. Not sports page interesting but nonetheless kinda cool & useful stuff.

The Democrats control the Executive and Legislative branches. At least until the next midterm elections in 2022 (ah the drama of the never ending election funding raising cycles). The Biden Tax Plan wants to reduce the estate tax exemption from the current 2021 limits of $11.7 million to $5 or $3.5 million. Every estate attorney and trust company were crushed with clients wanting to move assets out of their estate during the last 4 weeks of 2020 (trust me it was crazy around here). South Dakota trust law was a no-brainer for these clients for various reasons whether using completed or non-completed gifts.

“The estate planning door for gifting $11.7 million out of your estate is not closed in 2021. It is just smaller than in 2020.”

America’s founding fathers wasted no time to tax their new citizens at death. Starting in 1797 Congress “instituted a system of federal stamps[1]” that allowed property when transferred at death to be taxed. The “death tax” came and went over the next hundred years or so, based on the internal and external wars needing to be funded. With the passing of the 16th Amendment in 1913 giving Congress the power to “lay and collect taxes on incomes, from whatever source derived” which kept the tax collection good times rolling (Libertarians are not happy about now) with the passing of the Revenue Act of 1916 establishing the estate tax. Like any good deer tick, this estate tax has never been shaken from it's host - US citizens. It is interesting to note that domestic asset protection trusts were not a big discussion in the early part of the 19th century.

With 30 words the 16th Amendment gives Congress almost unlimited flexibility and power around taxes [side note: thankfully America is still a democracy and not a monarchy]. Historical precedents exist with Congress retroactively changing income taxes. Since America follows common law, inherited from the English legal system, precedents carry huge influence on new laws passed by Congress.

The 1913 Revenue Act [side note: not to be confused with the Revenue Act of 1916] implemented the income tax rules retroactively. This occurred with the new Revenue Acts in 1918 and 1926. Fast forward to 1993 and the Omnibus Budget Reconciliation Act of 1993 (i.e., higher taxes for individuals and corporations) enacted on 8/10/1993 but effective for tax years beginning after 12/31/1992. The Supreme Court opined on the “legality” of retroactive taxation with approving the Congressional power under the “due process” clause of the US Constitution[2]. Suffice to say, income and capital gains taxes can easily retroactively be changed with lots of precedents. Hybrid Domestic Asset Protection Trust (DAPT) income and capital tax changes will be equally affected. This will affect a host of estate planning ideas (e.g., CRT, GRATs, etc.)

“The Democrats, until the November 2022 mid-terms, may control the head in Congress but the Republicans control the neck.”

Congress has decided not retroactively implemented changes to estate taxes since the first version of a “death tax” in 1797. Past performance is no guarantee of future performance. Since laws require precedents, Congress may use rational and legitimate legislative purposes of raising revenue from those who can afford it (e.g., top 1% of US taxpayers). Very long and complicated cases which Congress could use for their argument but that would be a stretch for retroactively applying changes to estate tax laws[3]. Though the Democrats control the Legislative and Executive branches they still need a supermajority for certain changes. Biden knows first hand on the disastrous results Obama achieved in the first midterm (i.e., 2010) election results of his Presidency - Republican sweep. Biden has publicly stated he wants to avoid the same result during the 2022 midterms. Everyone knows estate taxes are not a revenue producer but red meat given to the voters. Expect a bipartisan approach and a rational focus on where the money exists - income and capital gain tax changes.

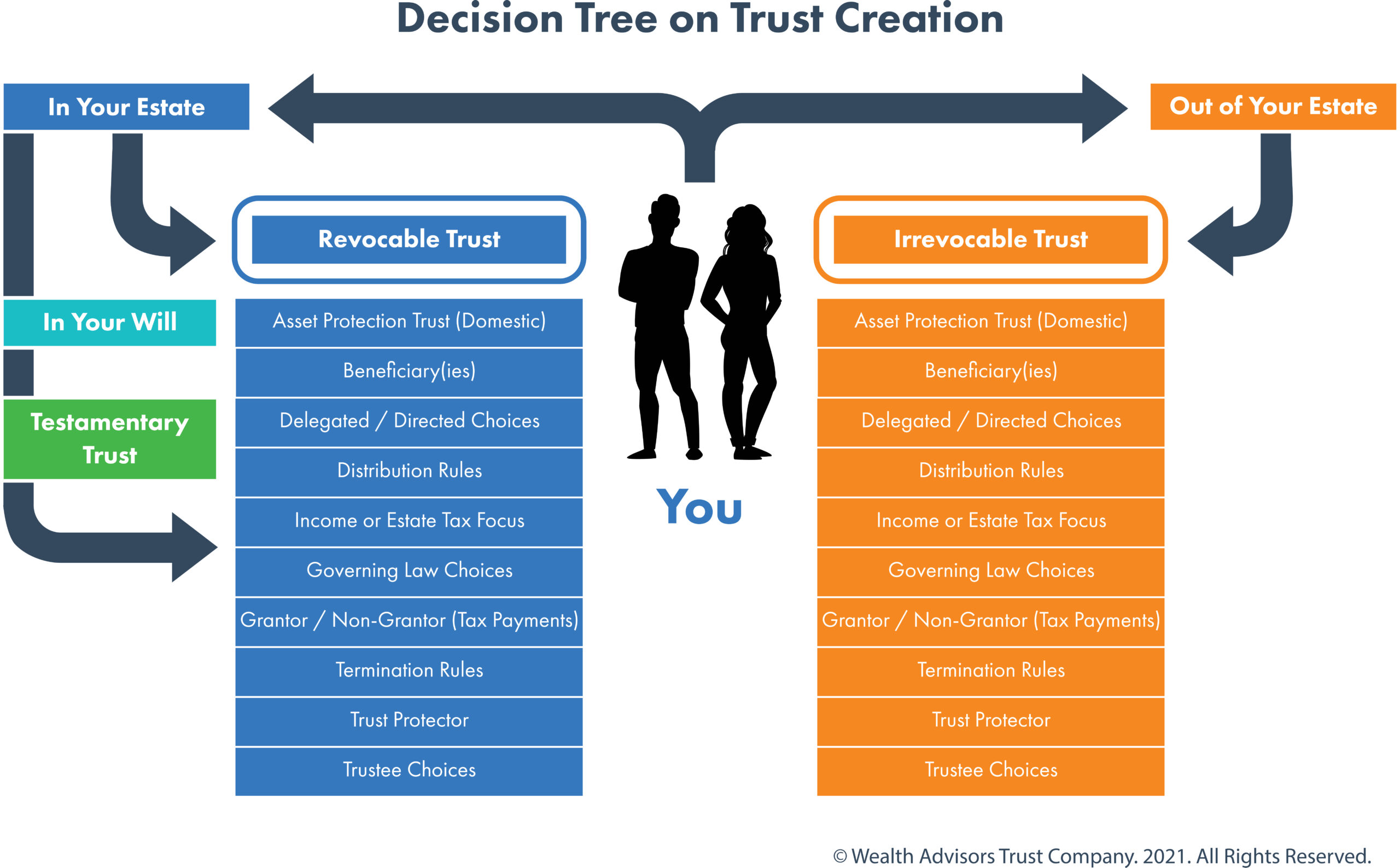

[Side note: For those well versed in trusts please skip to the Hybrid Domestic Asset Protection Trust (DAPT) section below for the interesting stuff]

The terms of an irrevocable trust must be set in stone. Situations can exist where certain items provide for a change (removal of trustees or change of the governing law for situs and trust administration). Very dependent on whether the trust statutes allow for non-judicial settlement agreement or require a court modification. The grantor, through creating the trust, basically gives up the right to use the trust assets and for the most part, control of those assets.

Beneficiaries of an irrevocable trust normally are the spouse and/or children. Could be anybody actually. Important to note that the definition of the spouse means whoever meets the definition of a legal spouse per state law. For those leaving high state income tax states (come on Governors, don't be shy, you know who you are) need to be mindful when their residency becomes effective on their new low state income tax home.

These trusts can exist for a specific period of time, the lifetimes of the grantor’s children or under a dynastic trust situation. Reasons for each of these terms can be dependent on the size of the trust, and/or the philosophical goal(s) of the grantor. Right and wrong answers do not exist for how long a trust should exist.

From a tax point, the irrevocable trust reason to exist could or could not be for income or estate taxes purposes. The trust could be considered a “grantor trust” by the IRS meaning that all the income and capital gains will be reported on the grantors individual tax return. This allows the trust assets to accumulate and the grantors taxable estate to be reduced further by paying the trust taxes. These type of trusts can also be a non-grantor trust for tax purposes. The trust would be a separate tax entity with a separate tax number. The possible advantages to creating a non-grantor trust, apart from domestic asset protection trust benefits, would be to remove the possibility of income tax being paid at the state level where you reside. Sorry folks - federal tax payments are a certainty not an option. Certain states such as NY and CA need extra attention to potentially mitigate the need to pay state income taxes.

The trust would typically remove the assets of the trust from the grantors estate for estate and gift tax purposes. Kinda a cool perk. Whether a grantor or non-grantor trust structure is used.

You guessed it - another irrevocable trust falling under the domestic asset protection statutes of South Dakota. This type of trust provides robust asset protection and efficient management of the trusts assets for the beneficiary(s).

A grantor creates and contributes the assets into the trust. The beneficiary of a traditional DAPT is most likely to be the grantor during their lifetime. There are various distribution provisions such as guaranteeing all the income plus 5% of principal per year, subject to the grantors own veto power over any proposed trust distribution. An independent trustee would have the discretion to distribute more than 5% of the principal per year.

Generally the term of the trust mirrors the lifetime of the grantor. The option exists to make the trust dynastic with the inclusion of contingent beneficiaries.

The trustee cannot be the grantor for obvious reasons. The option exists, with some legal drawbacks, for the grantor to be the investment trustee. One of the trustees must be a resident of South Dakota or a corporate trustee falling under South Dakota trust statute definition.

A South Dakota asset protection trust does not get created for any tax reasons. The trust has no income tax advantages or disadvantages per the IRS as it is structured as a grantor trust. The trust does not remove the assets from the grantors estate. Therefore, the assets that are in the trust at the grantors passing should be considered taxable under the taxable federal estate purposes (if applicable at all).

[Side note: This is the one great section for everyone]

A hybrid domestic asset protection trust (DAPT) falling under South Dakota trust law is a traditional irrevocable trust combined with a domestic asset protection trust. The Hybrid DAPT can be a non-grantor or grantor trust (e.g., glorified IDGT). Either way, the Hybrid DAPT removes assets from the grantor's estate. A trust protector has the power to add the grantor later as a permissible beneficiary (i.e., the escape clause) by creating a separate subtrust with the grantor as the beneficiary which would be included in the grantors estate but still offering domestic asset protection trust characteristics.

For CA and NY grantors the trust protector should not be resident of those two states.

Stated in another way, a Hybrid DAPT basically offers a traditional irrevocable trust where someone. the trust protector, has the power to add the grantor as a beneficiary by creating a separate subtrust. This is not accomplished via decanting but the Hybrid DAPT allows for the trustee to create a subtrust per the directions of the trust protector. As a rule of thumb, adding the grantor as a beneficiary would create a domestic asset protection inside of an irrevocable trust. Not bad for a day’s work.

If the grantor is not initially named as the beneficiary how can they access the funds if the subtrust is not created? Here are a few ways to access the trust cash flow if the grantor is not a beneficiary of the initial trust:

As a last resort, the trust protector could add the grantor as a beneficiary by creating a new subtrust allowed under the Hybrid DAPT language. This is not a decanting process, and no beneficiary involvement or court action is required. The trusts would currently fall under the DAPT statutes of South Dakota, assuming South Dakota trust law, and the trustee would split the initial trust into two separate trusts:

Why would we describe this topic? We want to be the corporate trustee when this type of trust gets created.

A Hybrid domestic asset protection trust (DAPT) has never been tested under South Dakota or federal law. It falls under the escape clause solution and not as the first place to go to solution.

For those grantors who want assets out of their estate they can use SLAT or IDGT solutions. A Hybrid DAPT solution gives them, the grantor, another option, should the situation arise where assets are needed back. Many grantors considering SLATs or other versions via an irrevocable trust are considering threshold questions about how to much to give away. Congress has passed retroactive income tax laws changes. They have never passed retroactive estate tax law changes. Past performance is not guarantee of future performance. The worse case scenario - the assets above the estate exemption amount are included back in the grantors estate. Not a bad outcome.

[1] Internal Revenue Service. Statistics of income Bulletin, 2007

[2] See Treatise on Constitution L. § 15.9(a)(iv), Retroactive Tax Legislation

[3] Guaranty Corporation v. R.A. Gray & Co, 467 U.S. 717 (1984); United States v. Carlton, 512 U.S. 26 (1994).