Finding cost efficient trustee fees frustrates many people. Wealthy and affluent people find using trustee services daunting.

Why?

Nobody understands the process of how corporate trustee fees calculations. Nobody understands exactly what a trustee does.

This 700 year old industry never had true external competition. No competition means no motivation for innovation.

Until now...

This definitive guide on cost efficient trustee fees will pull back the curtains on what corporate trustees do and how they charge their fees. With it, you can use a trust company with trustee fees on your terms. Our trustee fee schedule forces us to be effective and mindful.

Definition of a Corporate Trustee

Every corporate trustee uses terms people do not normally use, partly out of laziness and partly by design.

There are 7 different ways to describe a corporate trustee. This can lead to confusion for an individual and/or a financial advisor when you're looking for a trustee.

You need to understand the different types of a corporate trustee before you can decide on cost efficient trustee fees.

The matrix below provides definitions and examples of the 7 different ways a corporate trustee can be described.

| Name | Definition | Company Examples |

| Advisor Friendly Trust Company | A separate company that provides trust accounting and trust administration for personal trusts to financial advisors and beneficiaries. They do not invest trust assets, and they're typically based in top ranked trust states. They usually do not offer executor services required under someone’s will. | Known also as "independent trust companies." Examples are: Wealth Advisors Trust Company. |

| Bank Trust Company | A bank-affiliated organization that provides trust accounting and trust administration for personal trusts. They also provide executor services for people needing an executor for their will. These firms are connected to banks, and they do invest trust assets. | Known also as "traditional trust companies." Examples: CoAmerica, JP Morgan Trust Company, SunTrust, Frost Trust Company, Bank of America Trust Company, local or regional banks with a trust department |

| Trust Company | These companies are corporate trustees that can be affiliated or unaffiliated with a bank offering trustee services for personal trusts, such as revocable trusts, irrevocable trusts, and/or charitable trusts. | See examples for "Advisor Friendly Trust Company" or "Independent Trust Company." |

| Corporate Trustee | A corporate trustee is used in many situations, including personal trusts, escrow, retirement plans, corporate finance, structured finance, loan administration, public finance. |

Big banks offer most of these corporate trustee services. Examples are Bank of New York Mellon, BOK Financial Corporation, JP Morgan, Bank of America, etc. Some corporate trustee services for retirement plans are offered by niche players like Fidelity or Vanguard. Structured and corporate finance (e.g. issuance of bonds, maintenance of derivative contracts) corporate trustees are offered by State Street, Bank of New York Mellon, JP Morgan, etc. |

| Trustee Services | The duties, actions, and responsibilities an individual trustee or a corporate trustee must perform outlined in the trust document. These duties are based around trust accounting and trust administration. | Trust accounting, trust administration, and investment management. |

| Trustee | Used most often as a short phrase for anyone performing the duties outlined in a trust document for individuals. | A trustee could be a friend or family member, advisor friendly trust company, bank trust company, etc. |

| Independent Trust Company | These trust companies are not tied to a bank and offer corporate trustee services for personal trusts. They have the choice to offer investment trust services for personal trusts. |

Independent trust companies are segmented into two categories based on whether they offer investment trust services. Houston Trust Company is an example of one that does offer investment trust services. Wealth Advisors Trust Company is an example of one that does not offer investment trust services. |

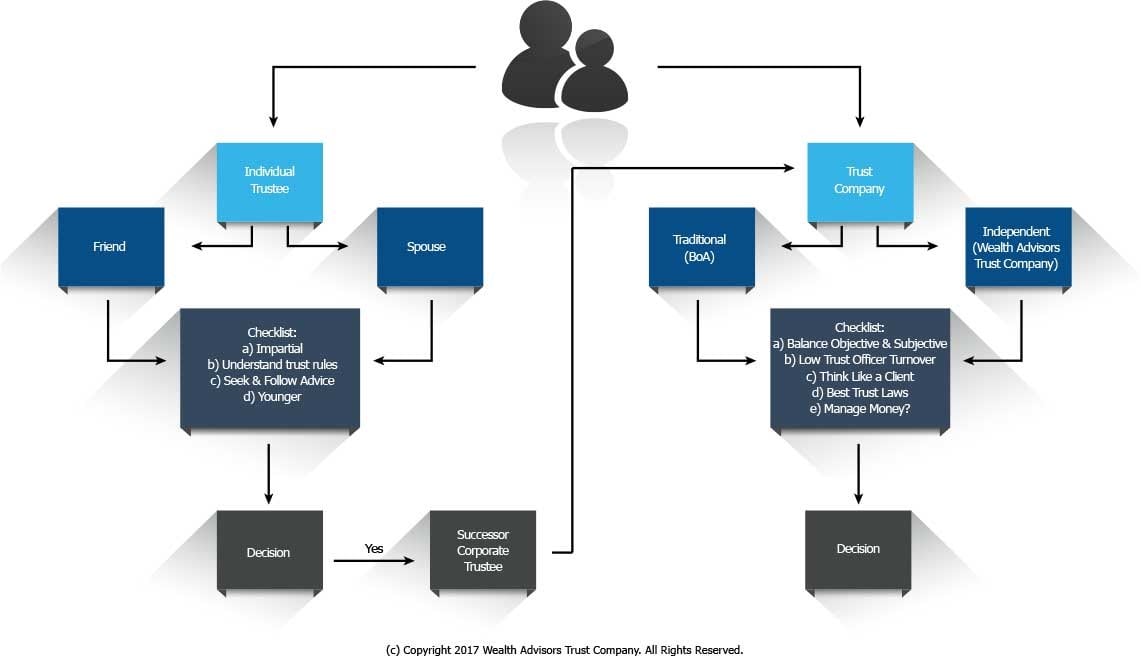

After learning this, most people have one big question they want to ask — how do I choose a corporate trustee for my personal trust?

The process of picking a corporate trustee can be narrowed to 4 easy steps.

If you want a corporate trustee, you have to choose whether you want them to invest or not invest trust assets.

After you select your trustee, you'll next have to discuss trustee fees.

But before negotiating cost efficient trustee fees, we need to know what a corporate trustee does for personal trusts.

Definitions of What A Corporate Trustee Does for Personal Trusts

A corporate trustee for personal trusts offers many services.

When you go into a restaurant, a menu provides a list of food choices and cost for each of those choices. We have the power to pick and to choose what we want against our budget for that meal.

Corporate trustees do not offer this type of transparency for their general trustee services.

Bank trust companies are especially guilty of this. Most advisor friendly trust companies and independent trust companies may not have this level of transparency either.

(However, innovative companies are challenging and changing this level of transparency over time in the finance industry.)

All corporate trustees do a solid job of listing costs for special trustee services like

- termination fees

- wire transfer fees

- meeting fees

- special asset review fees

Almost everyone using a corporate trustee does not get receive even a general layout of these fees.

They have no idea how trustee fees relate to trustee services. This makes it very hard for trustees and financial advisors to negotiate cost efficient trustee fees.

The matrix below provides definitions and examples of all the actions performed by a corporate trustee for personal trusts.

Trust Administration Table

| Duty | Actions | Who Does It |

| Distributions | · Collect document required backup

· Interpret trust document language regarding trust distributions · Interpret state laws, statutes, and codes · Provide adequate disclosure on statement descriptions · Disburse with proper allocation between principal or income · Interpret grantor’s intent |

Advisor Friendly Trust Companies: Trustee and financial advisor collaborate to determine outcome.

Bank Trust Company: Trust company determines outcome. Innovative corporate trustees provide the process to make this natural and easy, which helps with cost efficient trustee fees. |

| Investment Management | · Interpret and implement prudent investing

· Develop an investment policy statement/objective · Invest properly within the expected trust life expectancy · Invest appropriately with remainder beneficiary’s interest · Oversee/manage real estate, business interests, unique assets · Perform cash management · Buy/sell assets observing tax advantages |

Advisor Friendly Trust Company: Collaborative effort between Trustee and Financial Advisor. Bank Trust Company: Decision made by trust company. This materially affects trustee fees. |

| Trust Statement Generation | · Accounting is timely and accurate

· Include trust property entering or exiting the trust · Show all Receipts and Disbursements · Disclose all property administered with accurate descriptions · Cash balance with depository of where the balance is kept · Known liabilities owned by the trust · Separate Principal and Income accounting |

Any corporate trustee. |

| Trust Committee | · Meet as required by state law or needs of beneficiaries

· Approval of new trusts · Approval and document all purchases, sales of, and changes in trusts assets [Note: not if using an Advisor Friendly Trust Company] · Make periodic reports to the Board of Directors or to individual beneficiaries · Keep minutes of actions taken on individual trusts · Approval/Discuss/Document of discretionary distribution requests · Approve and document trust account closings · Conduct/document due diligence on financial advisors and third party vendors [Note: only if using an Advisor Friendly Trust Company] |

Any corporate trustee.

Innovative corporate trustees have internal processes to create supporting documentation, which helps with cost efficient trustee fees. |

| Tax Compliance | · Collect trust asset K-1s

· Collect all 1099s and investment tax accountings · Produce a tax worksheet · Adjust between Principal and Income when necessary · Complete and timely file trust tax return |

Any corporate trustee. Offering tax compliance without tax planning is like having a car without gas. Most corporate trustees only offer tax compliance. Advisor friendly trust companies (like Wealth Advisors) can offer both tax planning and tax compliance. |

Trust Administration Commodities

| Duty | Actions | Who Does It |

| Tax Reporting | · 1099 Generation

· Amortization/OID calculation · Wash Sale reporting and adjustments · Original Cost Basis/Original Face Value reporting · Proper Gain/Loss reporting |

Any corporate trustee or custodian that holds trust investment assets |

| Reconciliation | · Assets at Custodian

· Cash in bank and/or at Custodian · Physical property, where held and valuation · Income expected/received |

Any corporate trustee |

| Corporate Actions | · Calls, Maturities

· Tender Offers · Puts/Calls · Mergers/Acquisition/Spinoffs/Stock Splits · Class Action filing |

Advisor Friendly Trust Company: Delegated to financial advisor and/or custodian Bank Trust Company: Done internally |

| Principal and Income Accounting | · Separation of principal payments from income payments

· Separation of principal receipts from income receipts · Return of Capital · Interest/Dividend · Sales/Purchases/Paydowns · Capital Gains – should Short Term Capital Gains be applied to income or principal |

Any corporate trustee |

| Distributions | · Net Income

· How Often · Fixed Amount · Check/Wire/ACH – how they want it · When requested |

Advisor Friendly Trust Company: Delegated to financial advisor and custodian Bank Trust Company: done internally |

Cost efficient trustee services treat trust accounting as a commodity with a super focus on automation and efficiency. Imagine a trustee sending beneficiaries an invoice only for trust accounting. Nobody wants to overspend on this commodity type service. Disrupting and innovative corporate trustees relentlessly pursue efficiency on this front. This allows corporate trustees fees to be priced better for beneficiaries. Trust administration offers the secret sauce of any corporate trustee service for personal trusts. Look at the menu list. What was not included are Concierge Services, Meals and Entertainment, Corporate Events etc. Those trustee services find their way into every trustee fee.

(Note to reader: Wealth Advisors Trust Company does not offer concierge services, corporate events, or meals and entertainment for beneficiaries.)

The largest cost to any corporate trustee is risk, and that shows up in trust administration.

Cost Efficient Trustee Fees

Ask most people and they will tell you cost efficient trustee services exist only in a dream. This can be a reality for everyone. Every corporate trustee fee should rest on their risk and time. The goal for every current or future beneficiary should be to find that menu of trustee services. Pick the services you want and get use to cost efficient trustee services. The challenge comes when corporate trustees do not factor in cost efficiency. Either from a trustee fee standpoint or operationally at the company itself. They have never had real competition over the last 700 years. No competition means no pressure to innovate anything. The trick for beneficiaries and/or their advisors rests on peeling back the different components of costs. Some of the largest costs beneficiaries cannot "unbundle" are the soft trustee services. Examples are concierge services, meals /entertainment and corporate events. Would you want to pay for those soft trustee services separately? Should you have the choice to decide? The answer for the first question depends on your needs and the answer for the second question should be yes. The power to unbundle and to pick cost efficient trustee services depends on the type of corporate trustee used. Bank trust companies offer the greatest bundling of trustee services. Advisor friendly trust companies offer the greatest unbundling of trustee services. The right choice depends on the beneficiaries needs and wants.

Bank Trust Company - ideas for cost efficient trustee fees

A bank trust company has three distinct expense areas - investment management, trust administration, and back office operations. They separate their trustee fees between investment management and trust administration. Investment management fees for a trust account offer the greatest profit center to a bank trust company. The time involved for a $2 million trust account vs. $9 million trust account does not vary. The time involved should be considered as a fixed expense. Add more gross revenue to a fixed expense and the net profit rises exponentially. Beneficiaries of larger trust accounts pay more in investment management fees compared against the time involved. The trick for a bank trust company is calculating the risk for trust accounts. Assuming the trust owns marketable securities, the risk centers on under-performance, bad asset allocation and/or bad client service. The pricing of risk in any corporate trustee has qualitative and quantitative components. The quantitative components - the "riskiness" of the trust assets and the complexity of those assets. The qualitative components - the time involved in administrating the trust and dealing the trust beneficiary. Some beneficiaries carry more risk (e.g. never happy regardless of performance or service). To achieve cost efficient trustee fees layout the following: type of assets owned by the trust, number of contacts per year, and number of distributions per year. Ask the bank trust company to specifically layout the cost for those areas. If you do not want the other soft trustee services then ask for the unbundled trustee fee. The latter will be the hardest to achieve.

All bank trust companies showcase their trustee fees under an Asset Under Management model. For example, first $2 million is 0.85%, next $2 million is 0.75%, etc. Beneficiaries should ask for them to separate the trust administration from the investment management fees. Then separate the trust administration fees under the unbundled concept. These companies have not created separate factors for risk and time when providing cost efficient trustee services. They have not separated the soft trustee services between those that want them and those that do not [Note to reader - do you normally pay for things you do not want?]. The extra hand holding, tickets to special events, corporate events with notable speakers all cost money. If you want to have those extra services then you should pay for them. If you do not then why pay for them. These companies have the data to know the profit from every trust against all these extra services. If they do not have the data, then the disruptive bank trust companies will take business away from them with cost efficient trustee services.

Advisor/Client Friendly Trust Company - ideas for cost efficient trustee fees

An advisor friendly trust company has two distinct expense areas - trust administration and back office operations. The trustee delegates the trust investment function to a financial advisor. This type of corporate trustee only focuses on trust administration. Generally, they do not offer corporate events, unique speakers, and meals/entertainment services [Note to reader - We do not offer those soft trustee services]. However, they do offer their trustee services under an Assets Under Management fee model. Like a bank trust company they could charge 0.50% for the first $2 million, 0.40% for the next $2 million etc. Some of the them separate their fees for a delegated trusts vs. directed trusts. They carry the same worries of understanding risk and time with their trustee fees. The pricing of quantitative components deals with the complexity of the trust assets and time involved for trust administration. The pricing of qualitative components become easier because they do not hold themselves for offering those type of soft trustee services. The concept of cost efficient trustee services has not been a natural concept. Almost 100% of advisor friendly trust companies were founded by former bank trust company executives [Note to reader - not us. We are a former ex-Ernst & Young team]. When considering an advisor friendly trust company the trust fees can be easily separate between risk and time.

There are 7 distinct factors between risk and time:

1) Directed or delegated trust: A delegated trust, 95% of all trusts, means the trustee delegates the investment duties to a financial advisor. Yet they share the investment risk. In a directed trust, all of the investment risk rests with the financial advisor. Lower trustee risk equals lower trustee fees.

2) Type of assets: Trusts can own marketable securities, LLCs, partnerships, oil/gas, real estate etc. Dealing with unique assets comes at a great cost and expense. Trustees that place those unique assets into a manager managed LLC with the Members, excluding the trustee, having the power to select, fire and appoint the manager, can reduce trustee fees.

3) Custodian: An advisor friendly trust company does not custody trust assets. The financial advisor chooses the custodian. Some custodians have clunky data feeds and require more time for the trust reconciliation process. More time equals a bit higher fees (i.e. around 0.01% to 0.05% of increased costs).

4) Number of Beneficiaries: More beneficiaries take more time.

5) Number of annual distributions: Distributions can be separated between discretionary (approval required by trust committee) and standard. The more distributions that are standard the less time involved in trust committee approval and therefore less trustee fees.

6) Size of trust: This is all about risk. A higher trust size carries a higher risk to the trustee should something go wrong. No different than a $5 million house has a higher insurance cost than a $500,000 house.

7) Number of trusts: The more trusts under a trust relationship that a trustee deals with increases the time involved.

You want a trustee that separates these risk and time factors for accurate and transparent cost efficient trustee services.

Conclusion on Cost Efficient Trustee Fees

People have a broad range of options when needing a trustee. The importance for everyone rests on understanding the trustee costs and services offered. Some of those costs are mandatory (trust administration and accounting) and others are somewhat optional (e.g. soft trustee services). The challenge for any current or potential user of corporate trustee services for personal trusts lies in the lack of innovation in this industry. There are trustees working hard to disrupt and to provide innovative and collaborative solutions. Cost efficient trustee services start with admitting and understanding what you want from a trustee.